Spend Your Savings And Save Your Income

Wait a minute. “Spend Your Savings and Save Your Income?” This sounds a bit harebrained, and for some it may be.

However, for many business owners, it may actually make far more sense to spend their savings and save their income. In fact, there are times when we need to hit the reset button on our way of thinking. This is often true in the area of wealth management and wealth accumulation. For example, conventional wisdom often encourages us to only tap our savings as a last resort.

Nevertheless, for many professionals and business owners, conventional wisdom may be an impediment to wealth accumulation. In many cases, a superior financial strategy is to live off savings and save income. This approach can grow (not shrink) savings while simultaneously maintaining the same standard of living.

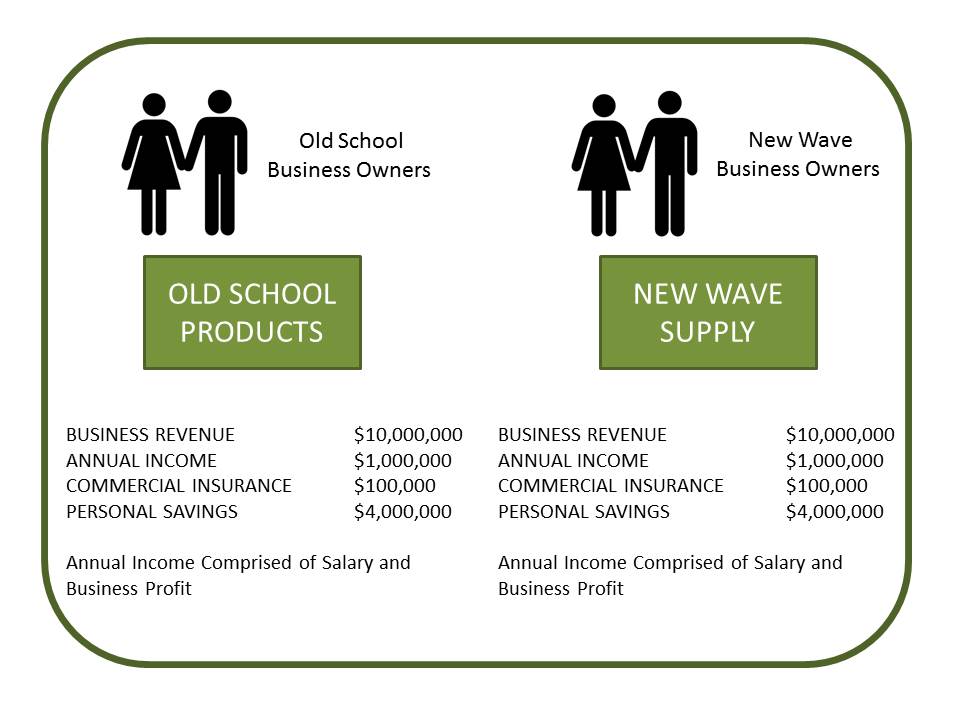

Consider the following example and illustrations below. Assume that Old School Business Owners (below) own a business that is identical to New Wave Business Owners (below). Figure 1 provides relevant information on their businesses and current financial situations. For this illustration, assume all other possible variables are identical.

FIGURE 1

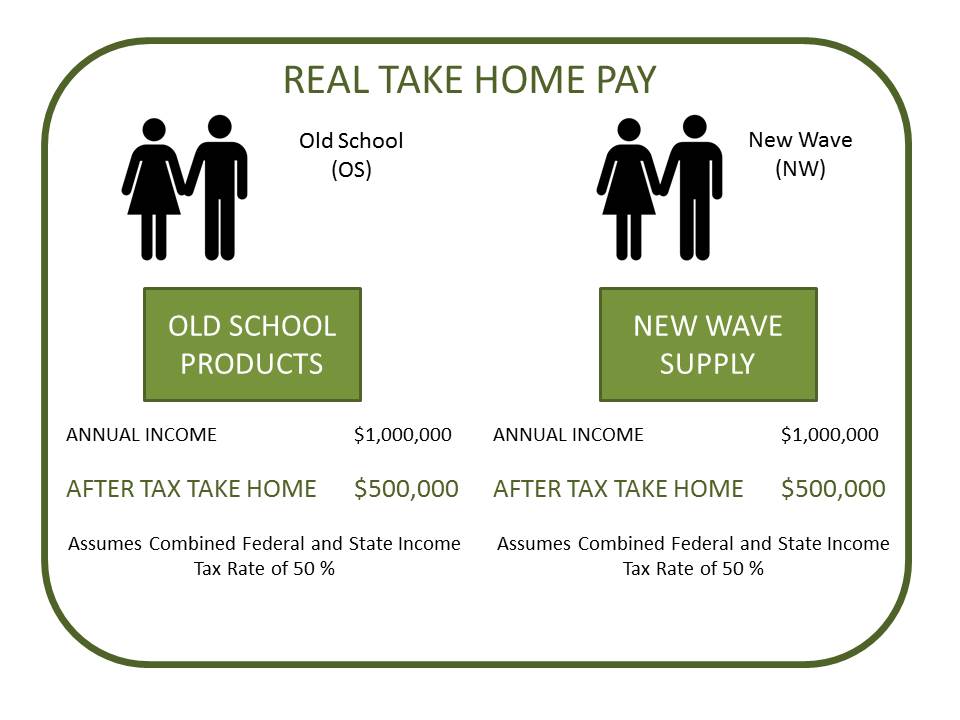

Old School (OS) enjoy the same standard of living (after tax take home pay) as New Wave (NW). Both sets of business owners spend $500,000 per year on their lifestyle as illustrated in Figure 2.

FIGURE 2

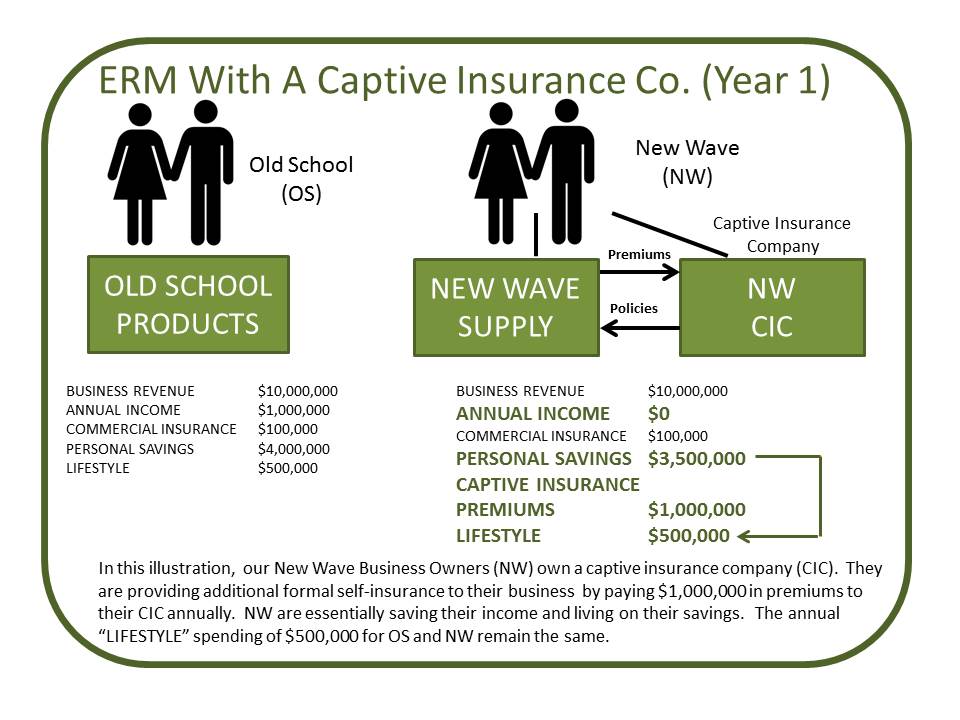

Figure 3 demonstrates that New Wave have decided to improve their risk management posture by implementing Enterprise Risk Management (ERM) and by owning a Captive Insurance Company (CIC). Captives form the backbone of ERM programs for small and mid-market businesses. ERM significantly improves risk management posture, making a business far more survivable. New Wave keep their commercial insurance coverage in place so their risk management profile is not altered. Their captive formally self-insures numerous other risks their business faces. It is important to note that New Wave own the captive insurance company, enabling them to also own the profits in the captive. Captive profits are defined as premiums received less claims paid. New Wave decide to spend their savings and effectively save their income. They accomplish this by drawing down savings (that has already been taxed) at a rate of $500,000 per year. They pay insurance premiums of $1,000,000 per year from their business to their captive insurance company. Their captive insurance company makes an 831 (b) tax election, and is taxed at 0% on its underwriting profits (premiums paid less claims).

FIGURE 3

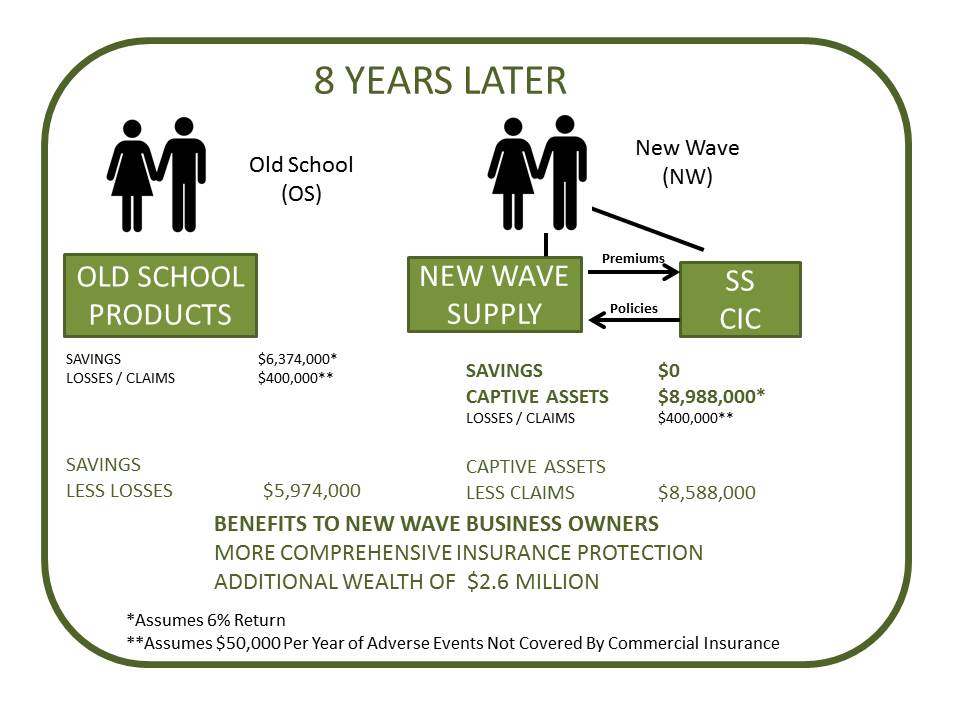

Figure 4 demonstrates the advantages to New Wave(NW) relative to Old School (OS) of spending their savings and saving their income. Over an eight year period, NW enjoy the same standard of living as OS, benefit from a more robust risk management strategy with greater insurance coverage, and accumulate additional wealth of $2.6 million. This illustration accounts for all fees associated with operating a captive insurance company (approximately $60,000 per year).

FIGURE 4

CIC Services, LLC is a full service captive insurance management company. We help business owners and professionals own their own insurance companies. A captive is a unique insurance company. It includes its own corporation, insurance license, reserves, policies, policyholders, and claims. It is a formal way for business owners to self-insure risk, and captives are generally formed to insure primarily though not exclusively the risks of one or more businesses owned by the same or related parties. Premiums are paid from the parent company to the captive with pre-tax dollars. The captive can invest its assets mostly as its owners choose (some domiciles have restrictions). Captives form the backbone of Enterprise Risk Management (ERM) strategies for small and mid-market companies. ERM is focused on survival. In addition to helping ensure survival, ERM also builds tremendous wealth for business owners.