ERM With A CIC Can Create – Not Just Protect – Significant Wealth For Business Owners

Is it possible to have a mature, leading edge business with an immature risk management strategy? The answer is a resounding “yes.” Many mature and successful businesses have an immature approach to risk management. The reality is that many small and mid-market companies survive and even thrive with immature risk management strategies, but many are leaving a lot of money – make that a ton of money – on the table.

Let’s face it, for many business owners and CFOs, risk management is not an enjoyable topic. It’s hard to get excited about risk management and insurance when one’s thoughts and energy can be focused on introducing a new product, or landing a new account, or entering a new market, or putting together a merger, or adding capital equipment, or securing a new facility. Also, taking steps to develop a mature risk management approach sounds like code for “spend more money.” However, the opposite is the case. Developing and executing a more mature risk management approach will almost always increase the total wealth of a business and its owners while better managing risks.

Entrepreneurial thinking has created tremendous wealth in the United States, fueled upward mobility, expanded the middle class and provided a standard of living that would have been unimaginable to America’s founders. This same entrepreneurial spirit gave rise to captive insurance companies (CICs) as enterprising businesses looked for a better approach to manage risk. In the early years, captives were primarily used to control insurance costs and ideally return a portion of premiums paid for insurance back to the parent company.

Beginning in the mid-80s, many businesses followed the entrepreneurial spirit and shifted their mindset from risk management simply as a form of cost containment to risk management as a profit center. Indeed, a more mature approach to risk management can be quite creative and entrepreneurial. Making the paradigm shift from viewing risk management purely as a cost center to viewing risk management as both a profit center and strategic pillar of the business can be very rewarding from a financial standpoint.

Critical to this paradigm shift is adopting a philosophy known as Enterprise Risk Management (ERM). Large corporations have employed ERM for some time, and this mature approach to risk management can also be adopted by mid-size and smaller companies. The backbone of an enterprise risk management approach is a captive insurance company (CIC). A CIC enables the business (or business owner or CFO) to take an active versus a passive approach to risk management. ERM increases depth of coverage and is a forward-looking approach to risk management. Furthermore, as a company’s ERM strategy matures, risk management can transition from being a cost center to serving as an entrepreneurial profit center.

A Mature ERM Approach Illustrated

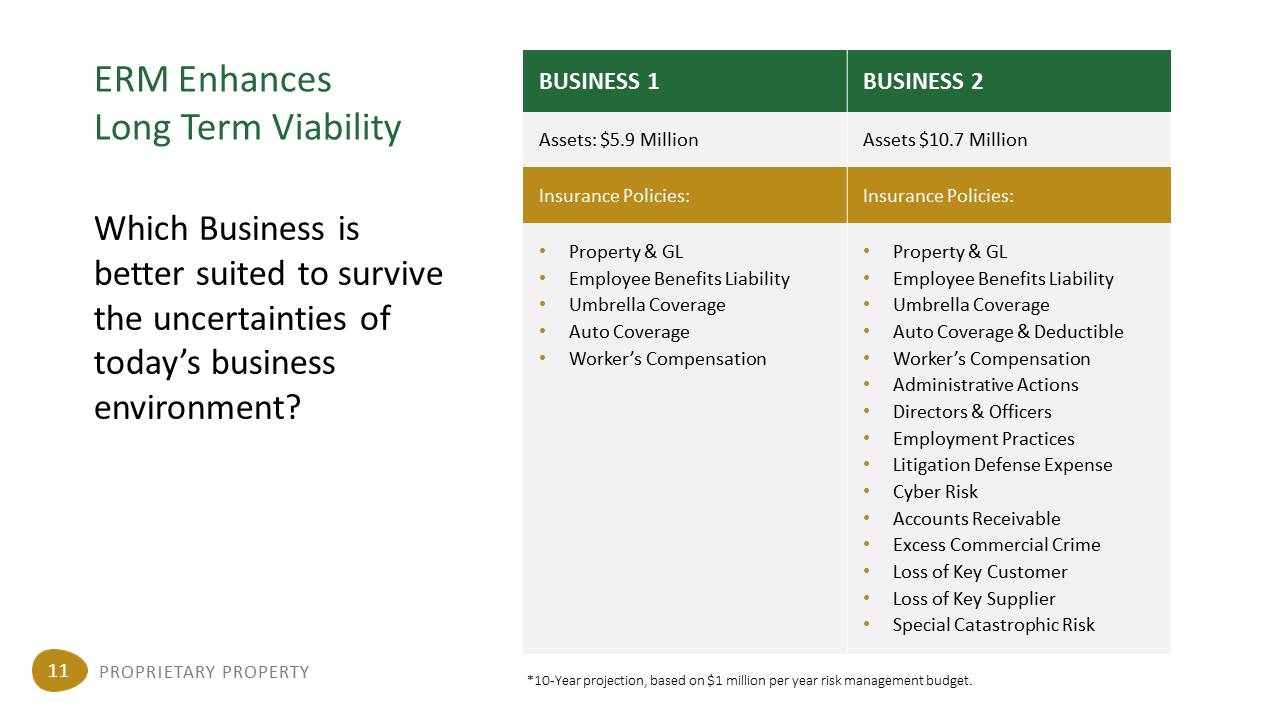

The impact of ERM with a CIC can be easily visualized by looking at the chart below, which depicts identical businesses over a 10 year period. The business on the left maintains the status quo with its immature approach too risk management. As can be seen, this business has less insurance AND less money. The business on the right adopts ERM with a CIC – a mature risk management approach – and enjoys more insurance coverage AND more money.

Ownership of one or more captive insurance companies makes ERM possible, because a business is able to both:

- Increase depth of insurance coverage

- Increase the time horizon of its risk management approach

Increase Depth Of Insurance Coverage

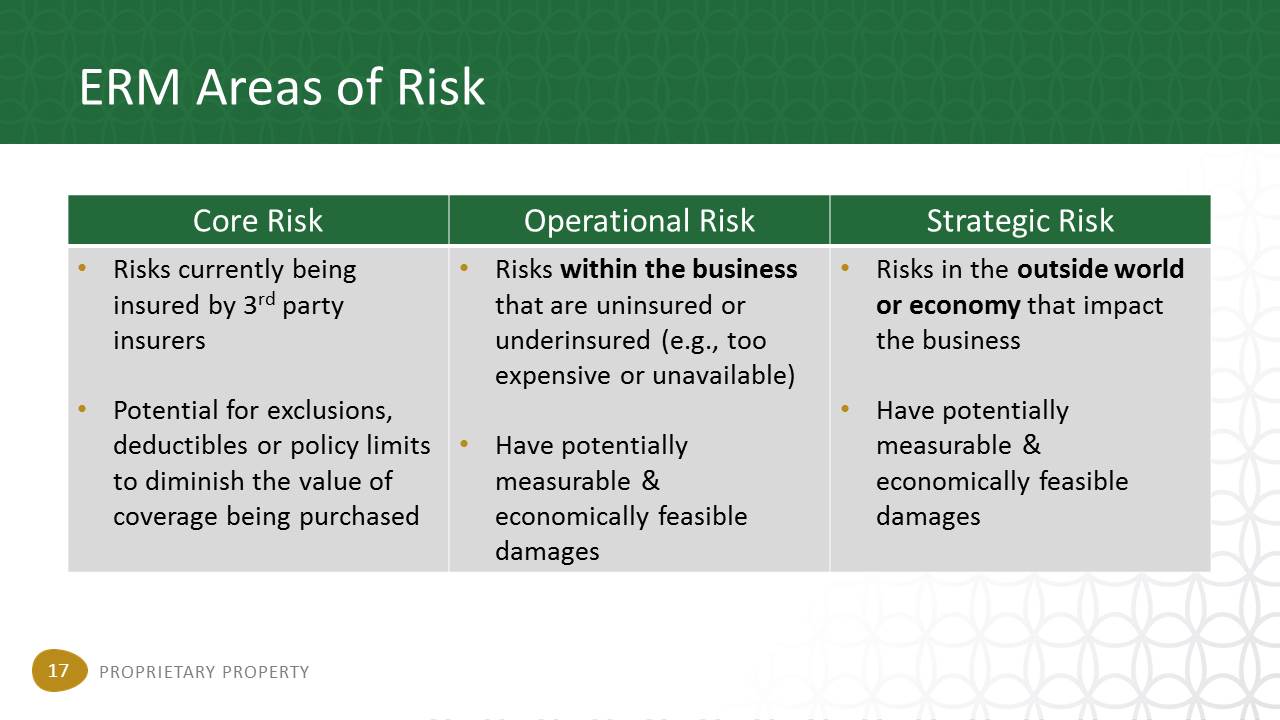

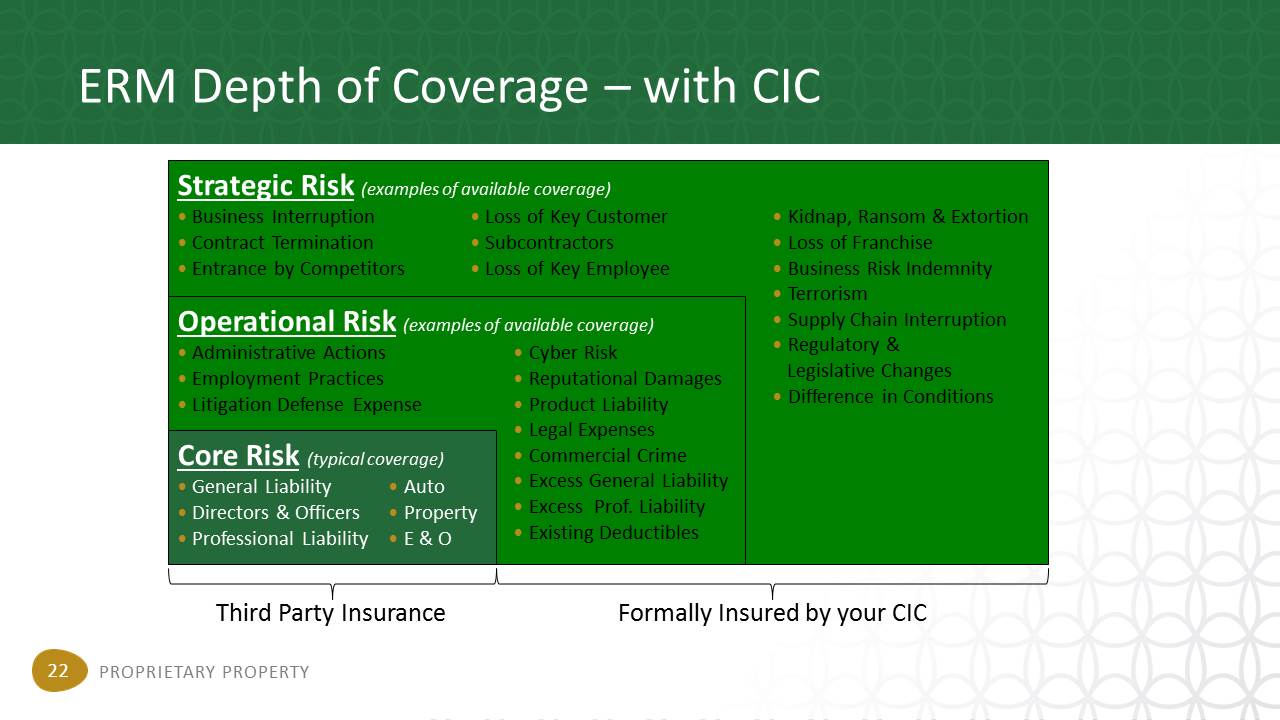

When employing a mature ERM model, risk managers and business owners categorize risk as core risk, operational risk and strategic risk (see the chart below). Most businesses and individuals simply insure core risk and usually do so via third party commercial coverage. Utilizing an ERM approach, a captive insurance company, in its formative years, gives businesses depth of cover by addressing the second and third layers of risk management (operational risk and strategic risk). As the captive matures and amasses reserves, it can also play a role in addressing core risk.

Quite often, operational and strategic risks can evolve into core risks. As an example, consider cyber risk. Many large corporations used to only address cyber threats as an insurable risk in their CIC. However, commercial insurers have caught up to the realities of the market and now offer third party commercial coverage for cyber risks. Now, many large corporations blend commercial coverage with coverage by their CIC to address cyber risk. Because of its flexibility, a captive insurance company will often insure risks that are difficult to cover via third party commercial coverage. Other examples include: supply-chain risk, extended warranties, loss of key customers and terrorism, as the chart below illustrates.

Increase The Time Horizon Of Risk Management

Another characteristic of a mature risk management approach is taking a forward looking stance. A short term approach to risk management typically views insurance as a year-to-year purchase with the goal of keeping costs as low as possible. Each year, all premiums paid for third party commercial coverage are a “sunk cost.” At the end of the year, if there are no claims, the money is gone. Because a captive insurance company is owned by the business owner(s) or the parent company, premiums paid to the captive insurance company are retained after claims are paid. Wealth accumulates in the captive as insurance reserves and provides flexibility to the business in its risk management in future years. A captive facilitates an ERM strategy because it enables a multi-year approach to risk management.

Financial Impact Of A Mature Risk Management Approach

Adopting an ERM approach with a captive insurance company as the chassis can be a financial game changer for business owners. Because the business owner and/or company can reap additional profits from its captive insurance company, the organization will inevitably make risk management and risk mitigation a higher priority. Furthermore, as the CIC grows its reserves, it is in a position to help reduce total reliance on third party commercial cover for core risks. This can often be achieved by reinsuring deductibles and insuring additional potential losses not covered by commercial insurance (including losses above third party insurance policy limits). Finally, CIC ownership enables the business owner or owners to capitalize on the favorable tax treatment that insurance companies receive on their reserves set aside for future claims. A well-structured ERM strategy with a CIC can save a business owner up to $1,100,000 per year in taxes.

Finally, employing ERM with a captive insurance company enables a business or business owner to capitalize on insurance law. Fortune 500 companies and other large company CFOs have been capitalizing on insurance law and tax treatment since the 1950s. The exact same strategies are available to small and mid-size companies. As part of its ERM, a business can purchase insurance from its captive insurance company (ies). Premiums paid to the captive are a tax deductible expense to the parent company. The captive insurance company receives the premiums in a tax-favored manner as a large portion are set aside as reserves for future claims. Reserves are not taxed, hence the insurance company is able to invest and grow a large pool of money. Insurance companies amass wealth by investing large amounts of pre-tax reserves. It’s also worth noting that if the insurance company qualifies as a “small” insurance company (defined as receiving annual premiums of $1.2 million or less), it can make an 831 (b) tax election and be taxed at a 0% (zero percent) rate on its underwriting profits. In 2017, the limit for “small” insurance companies increases to $2.2 million.

In conclusion, implementing ERM with a CIC can be a real financial game changer that TURNS RISK INTO WEALTH.