What Is a Captive Insurance Company?

A captive insurance company is a licensed insurance company owned by the business, business owner, or group of businesses it insures. Instead of sending all insurance premiums to third-party commercial carriers, a company can use a captive to insure selected risks through an insurance company it owns or controls.

For business owners, CEOs, CFOs, CPAs, and advisors, that ownership changes the insurance conversation. A captive can give a company greater control over how selected risks get financed, how premiums get allocated, how claims get handled, and how favorable loss experience benefits the business. Instead of treating insurance only as a recurring outside expense, a captive allows the company to own a meaningful part of the risk financing structure and connect insurance decisions more directly to liquidity, reserves, and long-term financial performance. AM Best found that rated captive insurers preserved an estimated $6.6 billion for their owners from 2019 to 2024, funds that otherwise would have flowed to the commercial insurance market.

Captive insurance is often described as a formal method of self-insurance, but that phrase only tells part of the story. A captive is a regulated insurance company with capital, policies, premiums, reserves, claims processes, governance, professional management, and regulatory oversight. It gives a business a structured way to insure risks it understands, funds, and manages, while creating the potential to retain underwriting gain that would otherwise remain with an outside carrier.

How a captive insurance company works

A captive insurance company works by connecting the operating business, the insurance policy, the premium, the insured risk, and the claim-paying structure. The operating company pays premiums for specific coverage. The captive receives a defined portion of those premiums, assumes a defined portion of the risk, supports that risk with capital and reserves, and participates in claim payments according to the program structure.

Some captives issue policies directly. In other structures, especially when a company needs admitted paper, certificates of insurance, contractual recognition, or the backing of an AM Best-rated carrier, the program may include a fronting carrier and reinsurance. This structure gives the business access to recognized insurance paper while allowing the captive to participate financially in the program.

In a fronted captive program, a licensed commercial carrier issues the policy to the operating business. That carrier provides the policy form, regulatory authority, claims infrastructure, and carrier paper needed for third parties that require proof of insurance from a recognized insurer. The fronting carrier then transfers a defined portion of the premium and risk to the captive through a reinsurance agreement.

Reinsurance is insurance for insurance companies. In this context, the captive acts as the reinsurer. It accepts a contractually defined layer of risk behind the policy issued by the fronting carrier. The fronting carrier may retain a portion of the risk, charge a fee, administer certain obligations, and provide access to its rating, licensing, and paper. The captive receives a portion of the premium and takes responsibility for the corresponding portion of claims.

This is the insurance structure behind the strategy. The policy may come from an AM Best-rated carrier. The risk participation may flow to the captive through reinsurance. The premium funds the program. The captive’s capital and reserves support its claim obligations. The business gains access to carrier-issued coverage while also owning a structure that can retain underwriting gain when claims experience is favorable.

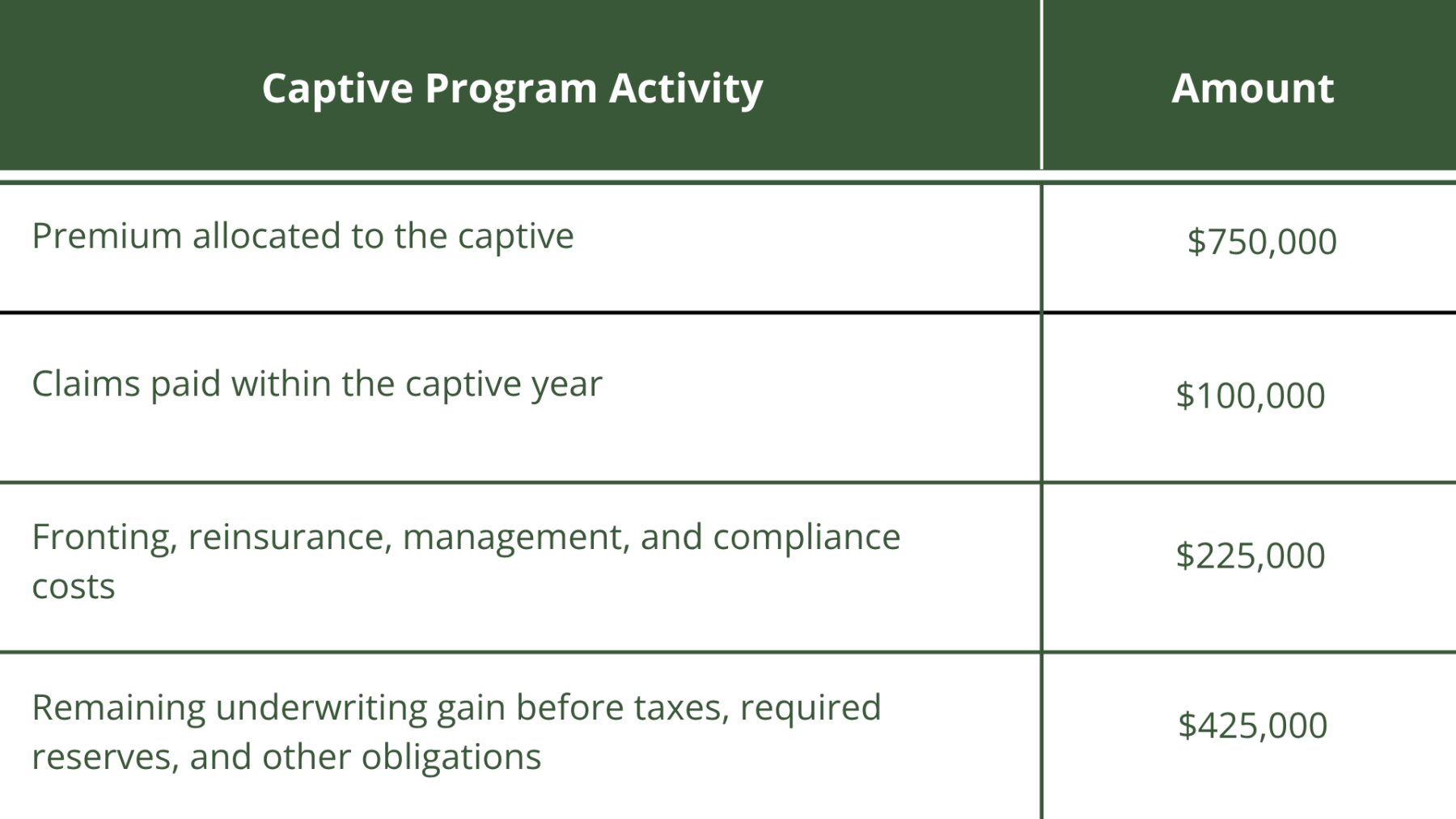

A captive insurance example with numbers

Consider a profitable middle-market company that pays $750,000 annually for coverage tied to certain business risks. In a traditional commercial insurance arrangement, the company pays the premium to a third-party carrier. If the company has $100,000 in claims, the remaining premium, after the carrier’s costs, reserves, and profit margin, stays with the carrier.

A captive structure changes that flow of premium. Assume the company participates in a fronted captive program. An AM Best-rated carrier issues the policy, which gives the company the recognized insurance paper it may need for lenders, customers, contracts, or regulatory purposes. Through a reinsurance agreement, the captive accepts a defined portion of the risk and receives a defined portion of the premium.

A simplified annual example might look like this:

In this example, the company has used premium dollars to fund an insurance structure it owns. The captive has accepted real risk, paid covered claims, covered program costs, and retained the remaining underwriting gain inside the captive structure, subject to taxes, required reserves, and other obligations.

That is one of the most important economic distinctions between captive insurance and a traditional third-party insurance arrangement. When claims are favorable in a commercial insurance program, the carrier generally keeps the underwriting gain. When claims are favorable in a captive structure, the business-owned captive can retain that gain and build a stronger reserve base for future covered losses.

For an owner or CFO, that creates a more strategic use of premium dollars. The company is not only purchasing coverage. It is also building a risk financing asset connected to its own claims experience, operational discipline, and long-term financial planning.

What a captive insurance company includes

A legitimate captive insurance company includes an insurance license, capital, policies, premium funding, reserves, claims procedures, regulatory filings, governance, and professional management. Depending on the structure, the captive program may also include a fronting carrier, reinsurance agreements, underwriting support, actuarial analysis, claims administration, accounting, tax guidance, and legal oversight.

Each component has a specific role. The policy defines the coverage. The premium funds the insured risk. Capital and reserves support the captive’s claim-paying ability. The fronting carrier, when used, issues the policy and provides carrier paper.

The reinsurance agreement transfers a defined portion of risk and premium to the captive. The captive manager and professional advisors help keep the structure compliant, documented, and financially sound.

This framework is what makes captive insurance more sophisticated than keeping cash on the balance sheet for possible losses. A reserve account can help a company preserve liquidity, but it does not create an insurance policy, a regulated insurer, carrier-issued paper, a reinsurance arrangement, or a formal claims process. A captive creates an insurance mechanism around risks the business wants to finance with greater discipline and control.

What types of captive insurance companies exist?

Captive insurance companies can take several forms, and the right structure

depends on the company’s goals, risk profile, financial capacity, and need for control.

- A single-parent captive, also called a pure captive, is owned by one company or ownership group and primarily insures that company and its related entities. This structure gives one business direct ownership and control over the captive and can work well when the company has enough risk, capital, and strategic need to support its own insurance company.

- A group captive is owned by multiple businesses that participate in the same insurance structure. These companies may share risk, expenses, and underwriting results according to the program design. A group captive can give participating companies access to captive insurance while spreading certain costs and risks across a broader pool.

- An association captive is typically formed for members of a trade association or industry group. This structure can work when businesses in the same field face similar risk issues and want an insurance solution built around the needs of their industry.

- A protected cell captive allows separate participants to insure risks within distinct cells of a larger captive structure. Each cell has separation of assets and liabilities, while the broader structure provides access to an existing captive framework. This approach can give a business a more efficient path into captive insurance when a standalone structure does not fit its goals.

These structures differ, but they share the same underlying concept: the insured business or participating businesses own or participate in the insurance mechanism, rather than relying exclusively on the traditional buyer-carrier relationship.

What makes a captive different from traditional insurance?

Traditional insurance transfers risk to a third-party carrier. The business pays premiums, the carrier issues the policy, the carrier handles covered claims, and the carrier retains the financial benefit when claims are lower than expected. The company receives coverage, but it has limited control over underwriting profit, policy design, claims philosophy, and long-term use of premium dollars.

Captive insurance allows the business to participate in that insurance function. The company can use commercial carrier paper through a fronting arrangement, participate in risk through its captive, and retain more of the financial benefit created by strong risk management and favorable claims experience. This creates a stronger connection between the company’s risk controls, its claims outcomes, and the financial results of the insurance program.

This is the financial logic behind CIC Services’ positioning around owning your own insurance company and turning risk management into a profit center. A captive creates the opportunity for profit by aligning premium, risk control, claims experience, reserves, and ownership within a structure that the business owns or controls.

Why liquidity and reserves are part of the captive conversation

For executives and financial advisors, one of the strongest reasons to understand captive insurance is the way it connects risk financing to liquidity planning. When a company sends all premium dollars to outside carriers, those dollars generally leave the business permanently. When a company allocates premium to a captive, a favorable claims experience can allow part of those dollars to remain within the business-owned insurance structure.

Those retained funds can build reserves that support future covered claims. Over time, the captive can become a more mature risk financing vehicle, giving the business a stronger funded position for selected risks. That can be valuable when a covered crisis creates a sudden need for cash, because the company has already funded part of the risk through an insurance structure designed for that purpose.

The captive’s funds must support insurance obligations, and the company must manage the structure properly. Even so, the reserve-building function can create a meaningful advantage. It gives the business a way to prepare for covered losses in advance, rather than waiting for a disruption, claim, or uninsured event to strain operating cash, credit capacity, or owner distributions.

Bottom line: What is a captive insurance company?

At its core, a captive is a business-owned way to finance risk with more control, structure, and long-term financial purpose than a traditional insurance purchase alone.

The operating company pays premiums into an insurance structure it owns or controls. The captive assumes defined risks, funds covered claims, and maintains reserves to support future losses. When claims experience is favorable, the financial benefit can remain within the captive rather than flowing entirely to the commercial insurance market.

That is why the answer to “what is a captive?” extends beyond a technical definition. For business owners, CEOs, CFOs, CPAs, and advisors, a captive is a regulated insurance company, but it is also a strategic financial tool. When properly formed, funded, managed, and regulated, it can help a business take greater ownership of selected risks, use premium dollars more intentionally, and connect insurance planning to liquidity, reserves, and long-term financial performance.